Markets

Wind Turbine Installation Vessels

Wind Turbine Installation Vessels

The changing global bottom-fixed offshore wind turbine and foundation installation market

By Philip Lewis, Research Director, Intelatus Global Partners

The last two or three years have seen a change in the underlying stakeholder support for the energy transition, resulting in the energy trilemma being focused more on energy security and affordability than transition, which means a pivot away from renewables to increased support for oil & gas. At the same time, inflation and interest rates have impacted project economics. Needless to say, these factors have impacted the global offshore wind forecast and the supply and demand balance for wind turbine installation and major component exchange (MCE) and foundation installation..

It is not all bad news. The UK and North Seas European countries are planning to increase offshore wind capacity (to increase energy security and affordability through scale) and advance grid integration (to manage localized offshore wind farm intermittency and stabilize the grid). Poland is advancing its offshore wind agenda. Mediterranean countries will enter the market. The big three EAPAC players (Japan, South Korea and Taiwan) will continue to advance offshore wind auctions and capacity development and will soon be joined by Australia and the Philippines. In North America (NAM) Atlantic Canada is looking to fill some of the hole left by the withdrawal of the USA from offshore wind, South America (SAM) is moving through the gears to establish offshore wind markets, and India (ISC) may soon turn plans into auctions.

This ever-changing market has an impact on the wind turbine and foundation installation market, where investment decisions for the latest generation vessels were generally made in more stable and promising times. As a result, utilization could be challenging, impacting day rates and financial returns.

These are some of the findings from a new bottom-up analysis and report by Intelatus Global Partners of the bottom-fixed turbine and foundation installation and maintenance market.

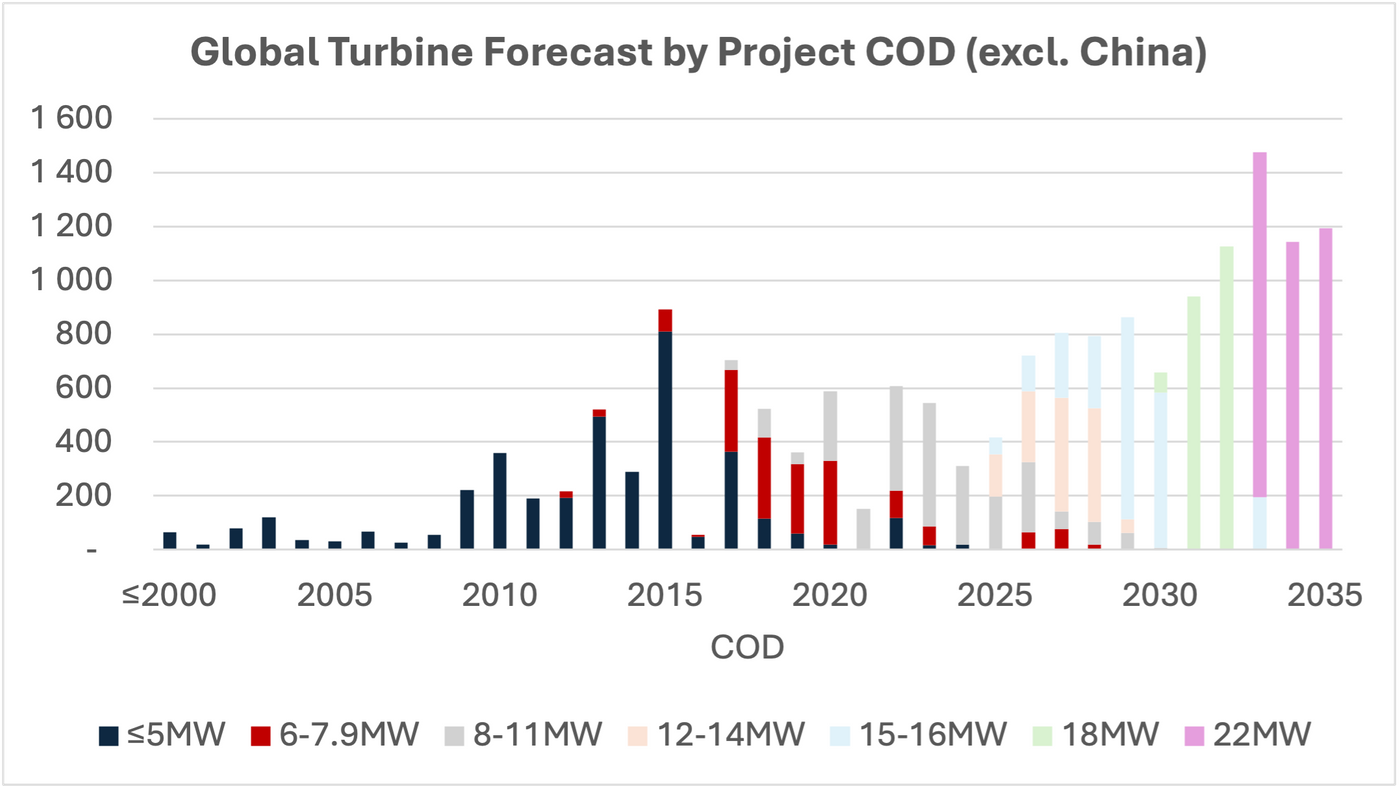

Changing demand has impacted the wind turbine and foundation installation supply & demand balance, resulting in tight to over-supply during the forecast period.

The global offshore wind forecast (excl. China) has “moved to the right” over the last year or so due to cancelled projects, disappointing auctions, cost increases and political headwinds.

The 2035 commissioned capacity forecast is ~230GW, of which over 90% features bottom-fixed technology. Europe accounts for over 70% of capacity additions and EAPAC 20%. In NAM, the project pipeline has been severely impacted by the current federal administration’s campaign against offshore wind projects and Canada looks to make a market entry in the next decade. Other new demand is forecast to emerge in SAM and ISC towards the middle of the next decade.

The 2035 forecast is ~17,900 commissioned turbines. Over 70% of turbines commissioned in 2025-2035 are forecast to be bottom-fixed. Europe accounts for ~70% of capacity additions and EAPAC ~20%. Forecast sensitivities include the speed of adoption of larger turbines and the speed of project capacity development.

The specialist FFIV segment (≥DP2 crane vessel with deck to carry several monopiles or jackets) excl. China will grow from 8 vessels to 9 by 2028 and is insufficient to meet global demand (excl. China) throughout the forecast.

Foundation vessel supply remains tight over several years of the forecast period when adding in foundation support from WTIVs. The FFIV and WTIV fleet is supported by 5 HLCVs and 4 HLSSs (≥DP2 crane vessel with a smaller or no monopile carrying capacity, often fed by barges, and also working in the oil & gas sector). Most can install XXXL monopiles and large jackets. At a granular level, the European FFIV and WTIV supply will struggle to meet all European foundation demand in the forecast period and requires HLCV and HLSS support. EAPAC is largely oversupplied with FFIVs throughout the forecast period, and both NAM and other markets are undersupplied throughout the forecast period.

As bottom-fixed turbine and foundation sizes are forecast to continue to increase, available WTIV supply (excl. China) capable of installing ≥15MW turbines is growing from none in 2020 to over 25 by 2028, made up of new generation high-spec vessels, designed to service larger wind farms built further offshore, and upgrades of earlier generation vessels. Supply is forecast to be able to meet global demand (excl. China) through the forecast period, although Europe is forecast to see tight supply in the ≥15MW segment from 2032 and from 2030 for other markets. EAPAC and NAM are oversupplied through the forecast.

The bottom-fixed WTMV fleet, both early generation WTIVs and oil & gas maintenance and intervention jack-ups, is forecast to stand at ~40 by end 2026 and is largely sufficient to meet major component exchange (MCE) requiring a jack-up intervention, subject to activity in the oil & gas market.

There are many sensitivities to the forecast, which can both increase and reduce vessel oversupply.

There are many sensitives impacting the forecast, including:

-

Timing and amounts of auctions of currently active markets and new players. For example, Germany has recently delayed its 2026 auction to 2027.

-

Grid connection availability.

-

Speed of adoption of larger turbines. The two leading western OEMs are currently focusing on turbines of ≤15MW, although Siemens is reported to be discussing commercializing its 20MW+ model for projects under construction in the next decade. Several Chinese OEMs are developing 16-25MW offshore turbines and a couple of discussing factories in the UK and Europe.

-

Acceptance of Chinese OEMs and scale of entry of Chinese installation and maintenance vessels to global the market. Chinese foundations, subsea cables and, to a lesser extent, turbines already feature in the European and EAPAC markets. Wide scale adoption of Chines turbines including planned European factories is still subject to significant political debate.

-

Cabotage/preference to build & operate domestic vessels, particularly in EAPAC and NAM.

-

Vessel productivity through technical capabilities of older/smaller vessels and newer/more capable vessels. New generation vessels achieve productivity of up to more than 40% compared to upgraded earlier generation vessels.

-

Changing economic returns (inflation, exchange rates, etc.).

-

Changing political support for offshore wind, as seen in the USA but it also witnessed in several other offshore wind markets.

-

Oil & gas demand for WTMVs, HLCVs and HLSSs for construction, intervention and maintenance.

-

Timing of industrialization of floating wind, which has generally moved further into the 2030s.

-

Black swans.

About the Author

Philip Lewis

Philip Lewis is Director Research at Intelatus Global Partners. He has extensive market analysis and strategic planning experience in the global energy, maritime and offshore oil and gas sectors. Intelatus Global Partners has been formed from the merger of International Maritime Associates and World Energy Reports.