Markets

Rigs

Caspian Sea Jackup Market: Locked-In Supply Shapes Utilization and Dayrates

In one of the smallest offshore drilling regions globally, a limited and locked-in fleet combined with campaign-driven demand continues to shape utilisation and dayrate dynamics. The Caspian Sea jackup market is among the smallest offshore drilling markets worldwide, yet it consistently exhibits some of the sharpest utilisation and dayrate swings. With no external supply response and a small, closed fleet, the market remains structurally tight and highly sensitive to timing.

by Sofia Forestieri, Senior Analyst at Esgian

Unlike larger jackup regions where scale provides greater flexibility, relatively minor changes in supply can have an outsized impact. The availability, reactivation, or retirement of a single rig can materially shift utilisation levels, dayrate negotiations, and contracting dynamics, often with limited visibility.

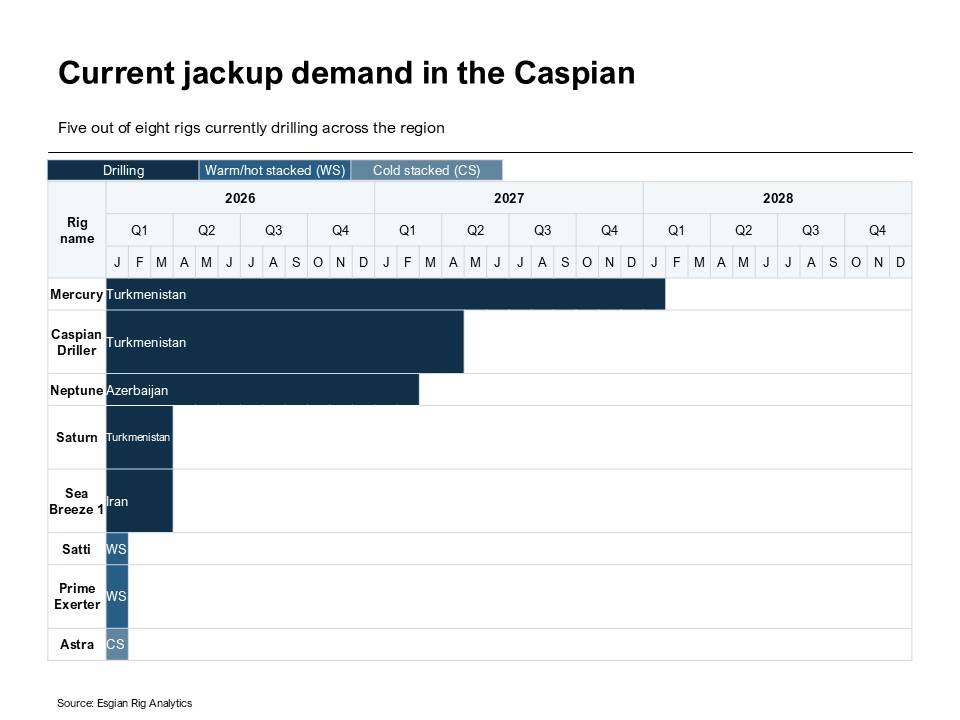

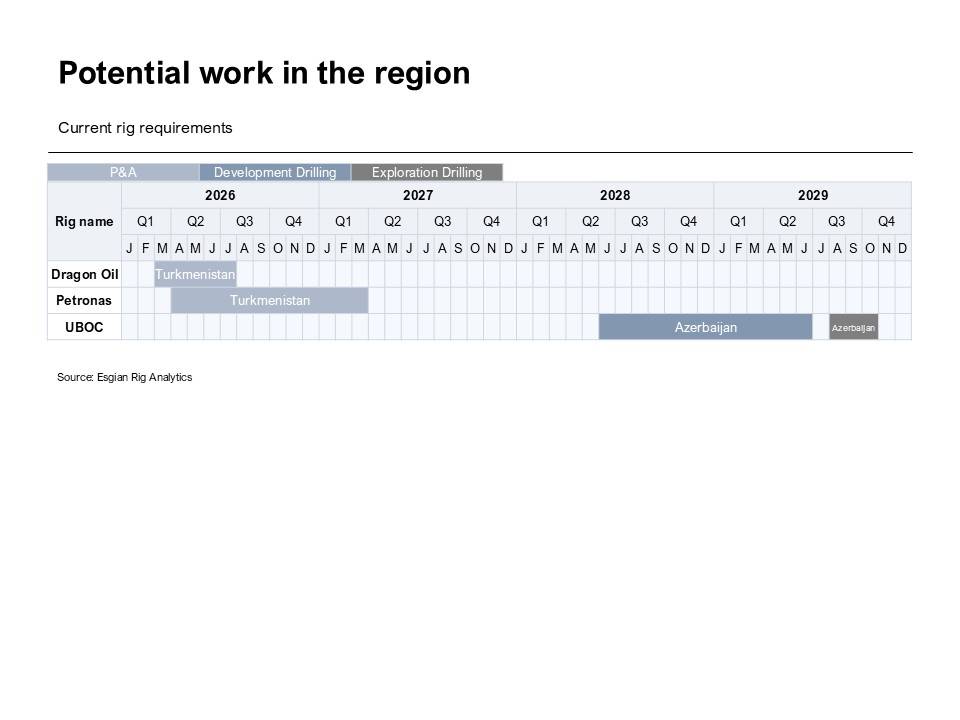

There are currently five jackups drilling in the region, operating across Turkmenistan, Azerbaijan, and Iran. Several of these units are contracted into 2026 and beyond, which is meaningful in a market of this size.

Despite this coverage, active supply remains constrained. Only two rigs, Satti and Prime Exerter, are currently available, while another unit is expected to roll off contract toward the end of Q1 2026. This leaves little spare capacity to absorb delays or unplanned work, reinforcing the importance of early contracting and campaign alignment. This tight supply environment also explains the high degree of regional rig mobility. Cross-border movements have become a defining feature of the market, reflecting both the absence of redundant capacity and the campaign-based nature of offshore programmes. While this mobility supports utilisation, it also introduces execution risk when projects are delayed, rescheduled, or reprioritised.

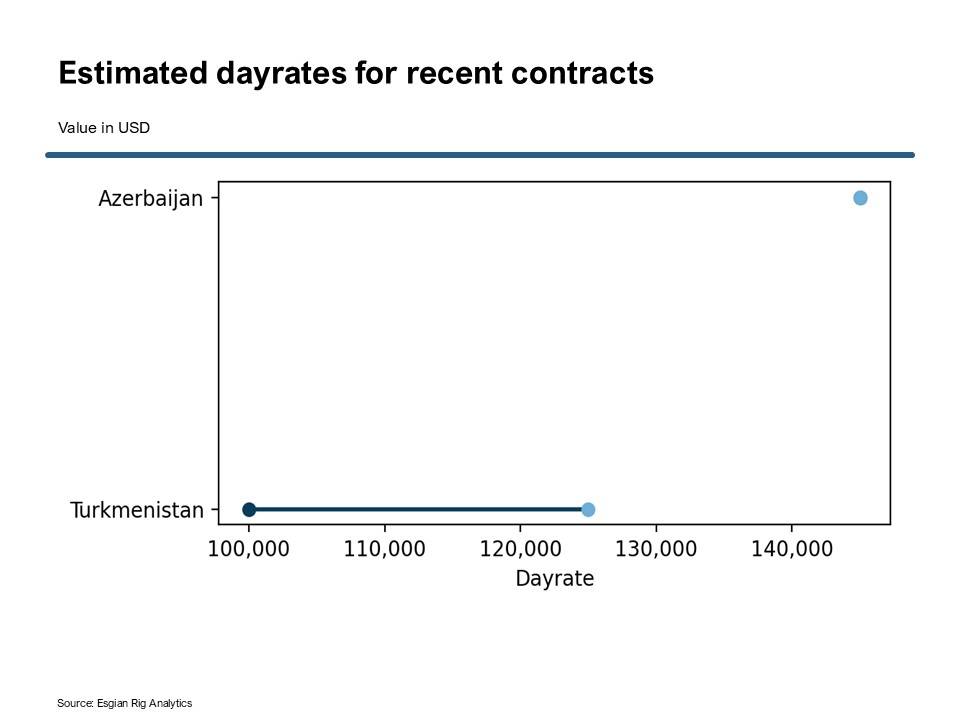

Dayrates are driven primarily by how many rigs are available at any given time, rather than broader global trends. Recent contracts have reportedly been fixed with dayrates above $120,000, levels that would be difficult to sustain in larger markets but can still be achievable in the Caspian under certain supply-demand conditions.

The small fleet size increases pricing volatility. When multiple contracts overlap, competition for a limited number of rigs can rapidly translate into stronger rates. On the other hand, gaps between projects can place downward pressure on pricing, even when longer-term demand remains intact. As a result, dayrates tend to move with individual projects rather than follow a stable long-term trend.

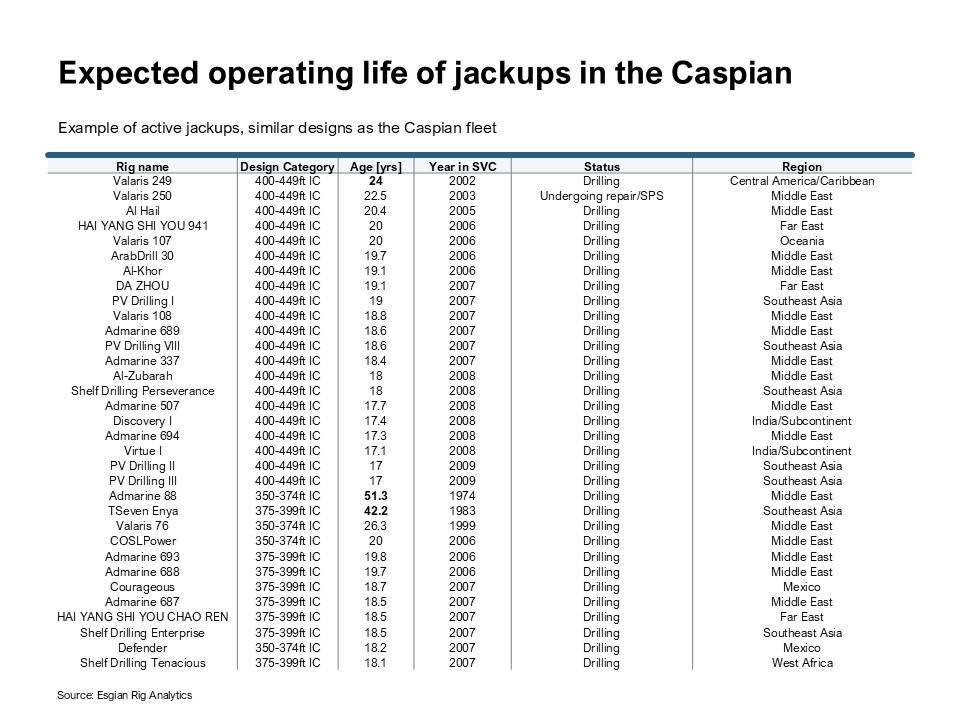

Although the Caspian jackup fleet is small, it reflects broader global trends in asset longevity. Many rigs operating in the region belong to design classes that continue to drill actively worldwide well beyond their original economic assumptions.

Globally, more than 120 jackups in the 400-449 ft IC design class remain active, with minimum working ages approaching 25 years. Comparable 350-374 ft IC and 375-399 ft IC design rigs show even longer operational lifespans, with several units continuing to drill beyond 40 years, and in some cases beyond 50. This suggests that jackups deployed in the Caspian are not constrained by near-term age limits. Instead, continued utilisation is more likely to be dictated by regulatory compliance, maintenance standards, and access to regional work rather than design life alone. Recent rig upgrades and the reactivation of Prime Exerter following a prolonged idle period reinforce this view.

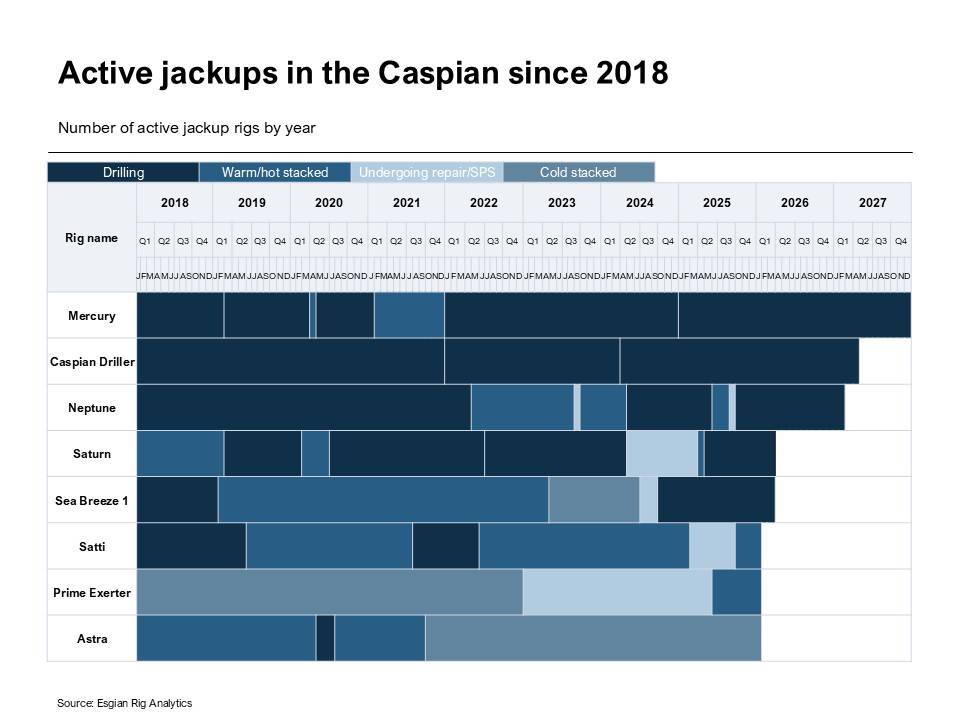

Earlier drilling in the Russian sector, led by Lukoil, gave way to renewed activity in Azerbaijan in 2021, before shifting toward Turkmenistan in more recent years. Today, demand is concentrated among a small group of operators, including Dragon Oil, UBOC, bp, and Petronas, reinforcing the market’s sensitivity to changes in capital allocation and project sequencing.

Caspian Jackup Market to Remain Stable and Structurally Tight

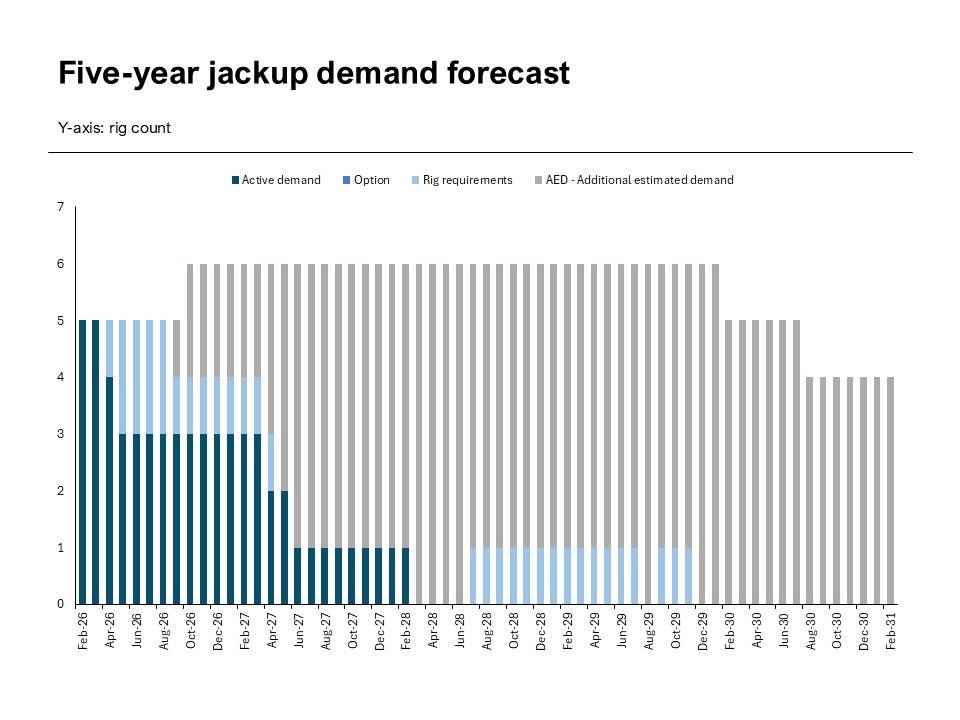

Looking ahead, jackup demand in the Caspian is expected to remain broadly stable at around five to six rigs over the next five years. While this does not point to structural growth, it implies continued high utilisation given the limited size of the regional fleet. Turkmenistan is expected to remain the primary source of demand, supported by ongoing offshore development activity.

Overall, the Caspian jackup market remains structurally tight and highly sensitive to timing. Limited fleet size magnifies both opportunity and risk: overlapping campaigns can shift dayrate negotiations toward contractors, while delays or cancellations can quickly affect utilisation.

In this environment, early planning and flexibility remain critical for operators, while rig owners continue to benefit from disciplined positioning and sustained regional access.

About the Author

Sofia Forestieri

Sofia Forestieri is a Senior Analyst at Esgian, specializing in offshore rig market analysis, energy economics, and sustainability. She has global experience in field operations and analytics.

©Esgian

©Esgian