Markets

Exploration

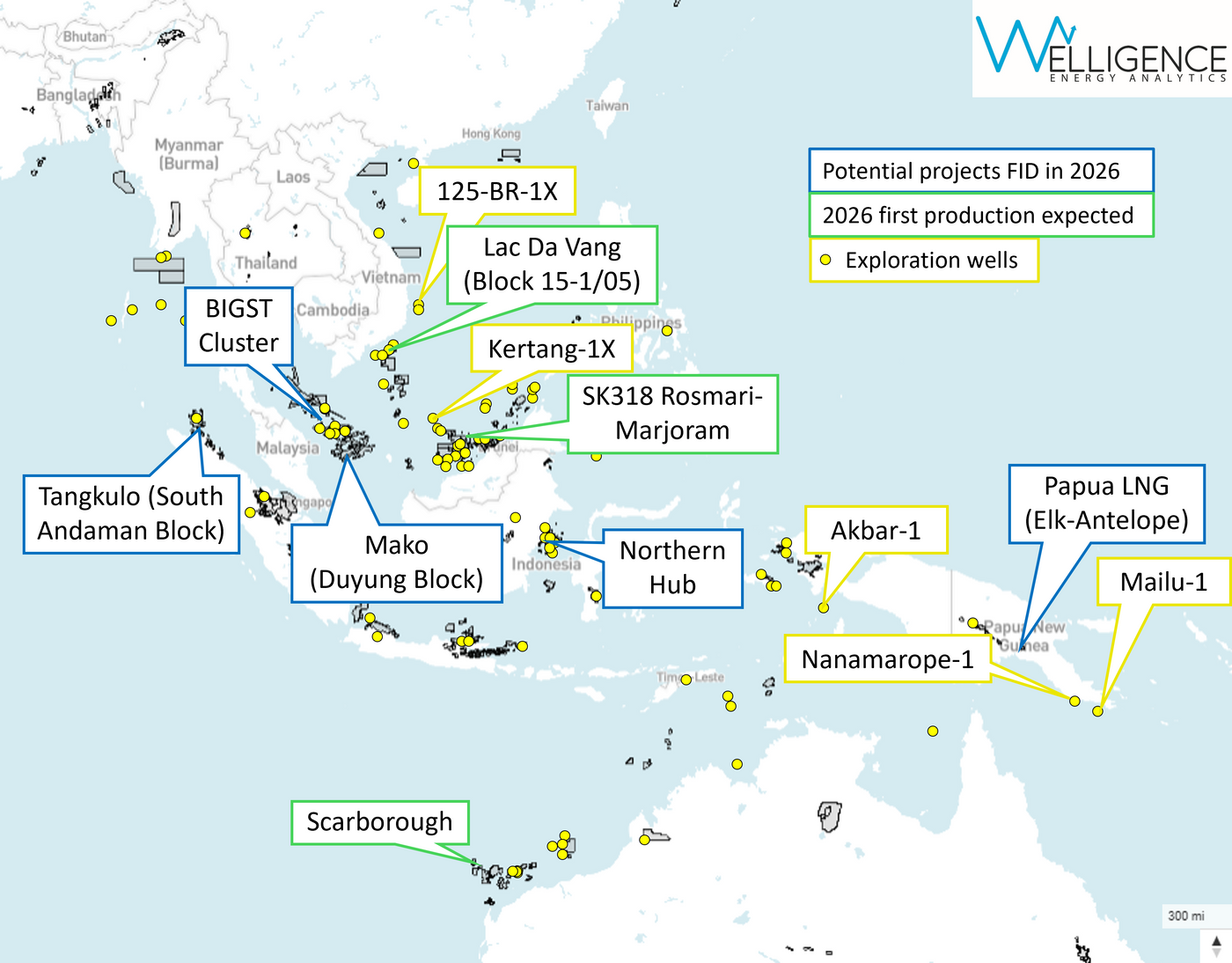

Asia Pacific Upstream 2026: Offshore Projects Ramp Up as Frontier Drilling Returns

Asia Pacific’s upstream sector heads into 2026 with a combination of near-term project delivery and high-impact frontier drilling. A wave of large offshore gas schemes is moving towards FID or first production, just as a new set of wildcats tests unproven deepwater plays. Together, they will shape regional energy security and LNG feedgas availability into the 2030s.

by JY Chew, Head of APAC Upstream Research at Welligence Energy Analytics

After years of investment, flagship oil and gas projects are now approaching start-up, while others vie for FID as governments prioritise domestic oil and gas and LNG supply. In parallel, operators are lining up potential basin-opening wells that could reset the region’s resource base.

Indonesia is at the forefront, repositioning offshore gas as a backbone for national energy security rather than purely for export. Mubadala Energy is fast-tracking the 2024 Tangkulo discovery on the South Andaman Block, with FID targeted by mid-2026 and first gas by late-2028. Domestic offtake deals are progressing, aligning the project with Indonesia’s drive to cut LNG imports and shore up local supply. The FID target at the Mako gas field on the Duyung Block is also 2026, with gas deliveries to the domestic market in late-2027.

Malaysia is following a similar path, with PETRONAS and ENEOS Xplora advancing the BIGST (Bujang, Inas, Guling, Sepat and Tujoh) cluster offshore Terengganu to deliver first gas to Kerteh by 2029. The project will reinforce Peninsular Malaysia’s supply base and support industrial demand as legacy fields decline.

Vietnam’s near-term offshore activity is more oil-weighted but still supports the domestic balance. Murphy Oil, with PVEP and SK Earthon, is targeting first oil from the shallow-water Lac Da Vang field (Block 15-1/05) by Q4 2026, using a new CPP and leased FSO. The 100 MMbbl field is expected to peak at 30,000–40,000 boe/d, helping offset Vietnam’s liquids decline and could re-energise exploration in the Cuu Long Basin.

Increasing APAC’s LNG Supply and Export Optionality

At the same time, project economics still hinge on long-term LNG offtake. New offshore gas developments are being configured to sustain or expand LNG exports.

In Indonesia, Eni is developing a large-scale Northern Hub development offshore East Kalimantan, anchored by the deepwater Geng North discovery in the North Ganal PSC and the Gehem field in the Rapak PSC, with a combined resource size of 6.6 Tcf of gas and 400 MMbbl of condensate. A new floating production facility with up to 2 Bcf/d of processing capacity is envisaged, feeding the onshore Santan terminal and supplying both Bontang LNG and domestic gas users.

Offshore Sarawak, Shell and PETRONAS are progressing the c.800 MMcf/d SK318 Rosmari–Marjoram sour-gas project, involving an unmanned wellhead platform, subsea producers and a 207 km pipeline to a new onshore sour-gas plant at Bintulu. The high-CO₂, H₂S-rich reservoir adds execution complexity and could push first production into early-2027, but the volumes are important for sustaining the Bintulu complex’s LNG output.

Papua New Guinea’s Papua LNG is the next major greenfield LNG project in Asia Pacific. Operated by TotalEnergies with ExxonMobil, Santos and ENEOS Xplora, it targets a 5.6 MMtpa development, producing from the Elk-Antelope fields (6-7 Tcf of gas). FID is targeted this year, with US$3 billion of EPC contracts or more planned, positioning the project as a key Asian LNG supply source.

Offshore Western Australia, Woodside continues to progress its Scarborough gas project. The deepwater field will be developed via a FPU and a 430 km pipeline to shore, providing feedgas to an expanded Pluto LNG complex. At plateau, Scarborough is expected to produce about 8 MMtpa of LNG, with first production targeted for H2 2026.

Across these schemes, the balance between domestic sales and export volumes will be critical. How this trade-off is managed in Indonesia, Malaysia, Papua New Guinea and Australia will influence LNG contract structures and pricing for years to come.

Deepwater Frontiers: Basin-Opening Wells to Watch

Alongside the near-term projects, exploration momentum is growing, with several deepwater and play-opening wells scheduled for 2026 and beyond. Success at any one of these would have basin-scale implications, materially expanding the region’s long-term resource base.

In Papua New Guinea, TotalEnergies and PETRONAS are preparing to drill the giant Mailu prospect in PPL 576 in the Coral Sea at c.2,000 m water depth. A discovery would improve the geological understanding of the broader area, opening a new play and de-risking adjacent clastic prospects. Also nearby in PPL 579, Larus

Energy’s Nanamarope-1 will test a different play concept but is contingent on securing a partner given the estimated US$100 million cost.

In Malaysia’s Block 2A, in the prolific North Luconia Basin, the Kertang-1X well will target Oligocene and Miocene formations in a very large four-way structural closure spanning more than 200 km² in 1,000 m of water. With c.5.2 Tcf of unrisked 2U prospective gas resources, a commercial discovery could underpin a wider deepwater exploration drilling campaign and a new LNG-scale development via the MLNG complex.

Vietnam’s planned 125-BR-1X well in Block 125 in the frontier Phu Khanh Basin is another standout opportunity, with unrisked mean prospective resources exceeding 13 bnbbl of oil across identified leads. Pharos Energy has secured a PSC extension to late-2027, but drilling will depend on rig availability and partner alignment.

In Indonesia, the Akbar-1 well in the Bobara Block off West Papua will be the first test of a frontier ultra-deepwater basin, operated by PETRONAS with Pertamina and TotalEnergies. A discovery would open a new play and support domestic production targets.

As 2026 unfolds, the region’s upstream narrative will be shaped by both sides of this story: a tangible wave of offshore oil and gas projects shoring up domestic supply and LNG exports, and several frontier wells, each potentially redefining longer-term opportunities.

About the Author

JY Chew

JY Chew is the Head of APAC Upstream Research at Welligence Energy Analytics, with over 21 years of experience in the upstream and energy industry. Prior to Welligence, JY held the position of Vice President at Rystad Energy, where he managed a research team covering Asia’s renewables and energy transition journey. He also served as a Senior Petroleum Economist at Wood Mackenzie, where he was a subject matter expert and led the upstream valuation products for Asia-Pacific.

©JY Chew

©JY Chew