Offshore Update

Marcon’s View of the Workboat World

Marcon International’s September 2024 Offshore Supply Market Report gives MarineNews readers a unique and up close snapshot of today’s workboat markets, and an in-depth look at the complicated Offshore Supply Vessel situation.

Of the 13,274 vessels and 3,730 barges Marcon tracked as of late September 2024, 2,776 are supply and tug supply boats, with 161 officially on the market for sale. 35% of foreign and 65% of U.S. flag supply / tug supply boats Marcon has officially listed for sale are direct from Owners. In addition to those for sale, Marcon has 52 straight supply and tug supply vessels listed for charter worldwide.

1,163 of the vessels tracked by Marcon as of late September 2024 are crew, fast supply & pilot boats with 133 officially on the market for sale, plus 38 boats are available for charter worldwide. 49.6% of the boats officially for sale are U.S. flag. Nineteen crew boats for sale worldwide were built within the last 10 years. Forty-six boats, or 34.59%, are 25 years of age or older. The oldest boat listed is a 40', 240BHP 1957 built and located U.S. West Coast. This vessel is counterbalanced by three 2020 built, foreign flagged 59' to 128' crew boats.

Market Overview

Tug supply boats officially on the market for sale listed with Marcon in total is 49, 17 fewer than September 2023 and 77 fewer than September 2019. Composition now versus five years ago has changed with dropping 70 AHTSs in the 3,000BHP to 8,000BHP ranges, with losing 20 in the 5,000 - 6,000BHP category alone. The largest change compared to last year was losing eight in the 5,000 - 6,000BHP category. September 2019, the average age of all AHTSs for sale was 15 years old, where U.S.-flag vessels averaged 29 years and foreign-flag AHTSs averaged 14 years. Today, the average age is 17 years old, with U.S.-flag AHTSs averaging 23 years and foreign-flag averaging 16 years old. At the time of this report, nine, 18.37%, tug supply boats officially for sale were either built within the last 10 years, including a newbuilding re-sale. Coincidentally, 18.37%, or nine, of tug supply boats are 25 years of age, compared to five years ago, when 16.67% of AHTSs for sale were at least 25 years old; and one year ago, 19.70% were at least 25 years old. Five years ago, 50.0% AHTSs listed were less than ten years old, whereas last year, this dropped to 21.21%. At September 2024, the oldest AHTS available from Marcon was a 1976-built, 194', 5,750BHP foreign flag AHTS located in the Caribbean. This is counter-balanced by a newbuilding re-sale 239', 8,000BHP foreign flag AHTS located in the Far East.

At 112 platform supply vessels listed for sale late September 2024, we have 29 fewer PSVs listed for sale compared to one year ago and 45 less than listed five years ago. Looking at change in vessel size composition over the past five years, the largest decreases were in the under 150' LOA (down 8); 150'-160' LOA (down 16); 170'-180' LOA (down 5); 180'-190' LOA (down 9); and 190'-200' LOA ranges (down 16). These changes were offset by a 15 vessel increase in the 220'-240' LOA range. PSVs now being offered are slightly older than those offered back in September 2019 with the average age of all available for sale at 22 years old compared to 20 years old then. U.S.-flagged PSVs decreased from 24 years to 22 years, while foreign flagged increased from 15 to 23 years old. As of this report, Marcon officially has available ten supply boats built within the last ten years, with no newbuilding resales listed. Forty-six PSVs, or 41.07%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 35 PSVs (24.82%) were older than 25 years and 17 PSVs (12.06%) were ten years or under, with no newbuild resales listed. Five years ago, 44 PSVs (28.03%) were older than 25 years and 35 PSVs (22.29%) were built within the prior ten years. Of those 35 PSVs, three or 2.00% were newbuild resales.

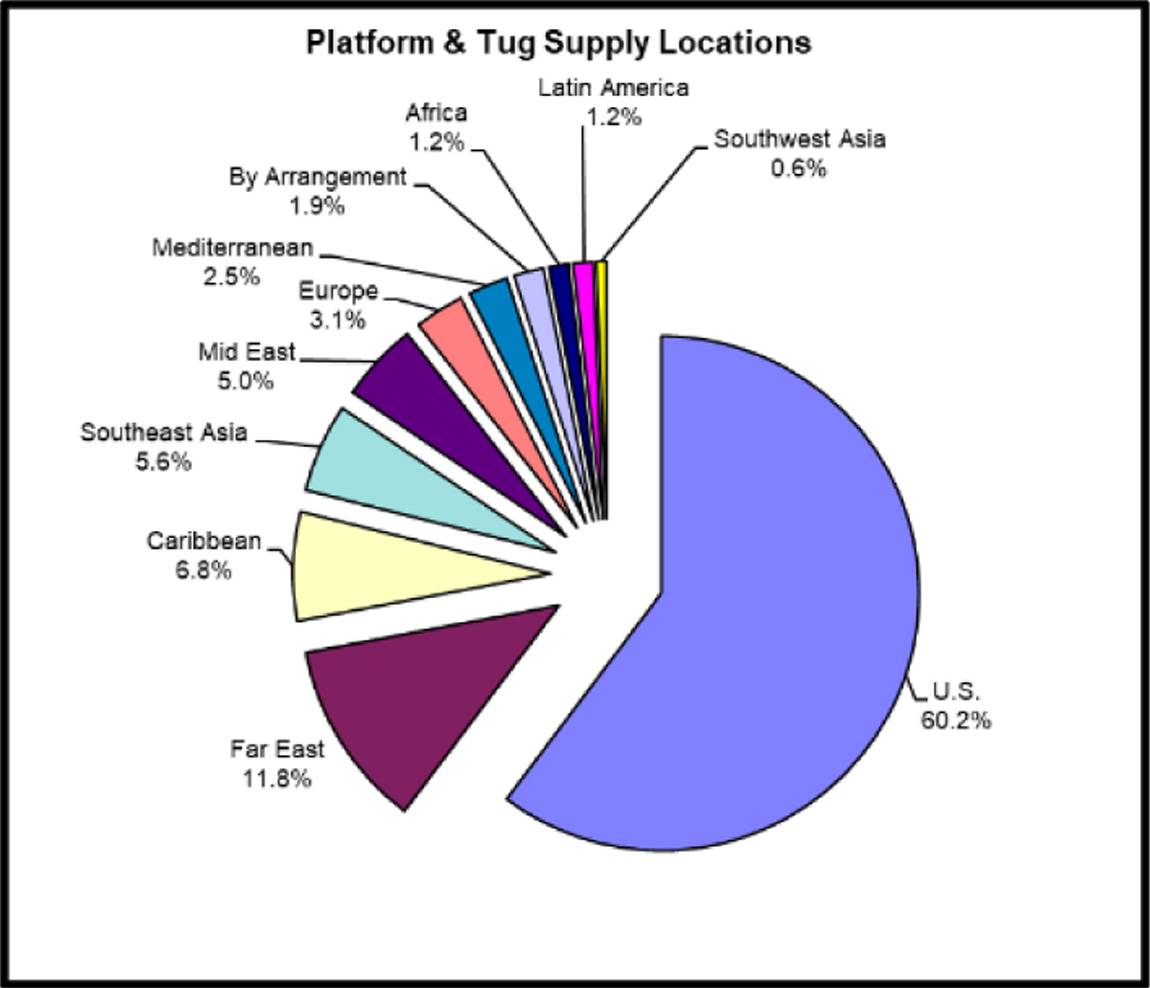

The dominant location for second-hand tonnage on the market September 2024 is the U.S. with 60.2% (up from 51.2% one year ago and 36.7% five years ago) followed by the Far East with 11.8% (compared to 8.2% last year and 11.3% in 2019), Caribbean 6.8% (5.8% in 2023 and 4.6% in 2019), Southeast Asia with 5.6% (down from 13.5% one year ago and 14.1% five years ago), Mid-East with 5.0% (6.3% in 2023 and 9.2% in 2019), Europe with 3.1% (compared to 3.4% one year ago and 5.7% five years ago, respectively). Where location is unknown is 1.9%. The rest of the globe makes up the final 5.6% of locations. CAT is the principal main engine supplier to this sector powering 90 (56.6%) of the 159 supply & tug supply vessels listed for sale where engine make is known, followed by Cummins in 19 (11.9%), nine each with Bergen and Wartsila (5.7% each) and seven (4.0%) each with EMD and Niigata. 18 (11.3%) units are powered by ten other manufacturers. Compared to five years ago, the percentage of available for sale PSVs and AHTSs powered by CATs increased by 21.9 percentage points, while those powered by Bergen dropped 5.5pp, EMD dropped by 4.9pp, Cummins declined 4.5pp and Niigata decreased 4.2 percentage points.

Crew boats officially on the market now are down 15 and 92 from one year and five years ago, respectively. In terms of vessel size by LOA available compared to five years ago, we saw the most significant declines with a 16% change in 30'-40' LOA, 39.1% drop in 40'-50' LOA and 110'-120' LOA crew boats dropping 12%. As of this report, 14.29% of the crew boats available are less than 10 years old, down from the 16.89% and 26.67% reported one and five years ago, respectively. Conversely, 34.59% today compared to 37.16% last year and 32.89% five years ago are 25 years or older. Five years ago, the average age of all on the market through Marcon was 21 years, the same as of this report, both only one year less than last year's 22 years old average. U.S.-flagged vessels historically are older than foreign flagged vessels listed by Marcon. Though the average age of US-flagged vessels as of the report date is 24 years compared to 27 years and 29 years, one and five years ago, respectively. Foreign flagged crew boats' age fluctuated over the past five years from 15 years five years ago to 16 years old last year, back up to 18 years currently.

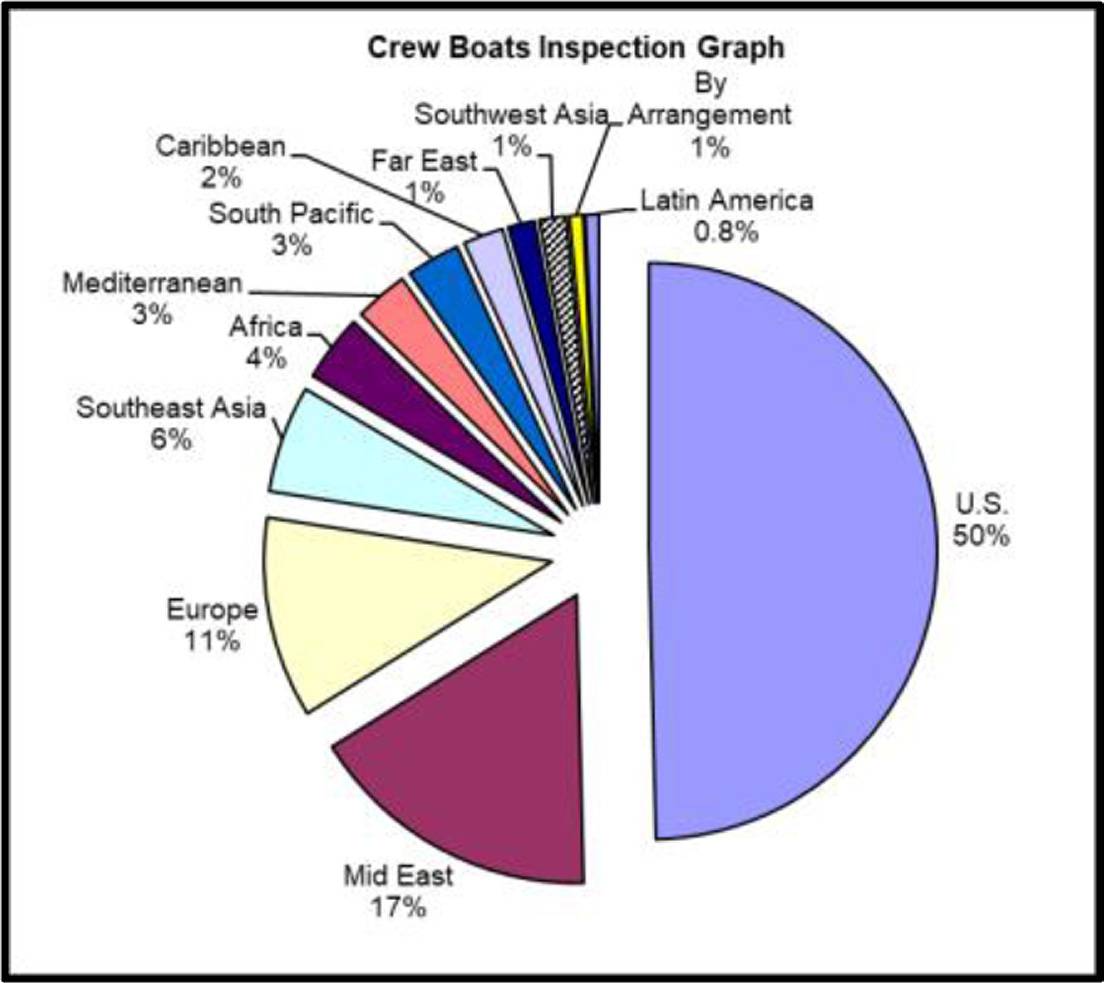

The dominant location for second-hand tonnage on the market September 2024 is the U.S. with 50% (same as one year ago and up from 41.8% five years ago) followed by the Mid-East with 17% (compared to 11.5% last year and 10.2% September 2019), Europe with 11% (vs 10.1% last year and 9.3% five years ago) and Southeast Asia with 6% (down from 15.5% one year ago and from 15.1% five years ago). Where location is unknown is 0.8%. The rest of the globe makes up the final 15.8% of locations. Of the crew, pilot boats and launches listed, the most popular engine is CAT in 65 of 131 boats where engines are given, followed by 25 Cummins, 18 GM/DD, MAN-B&W with five, four with MTU, and 14 under other types, ranging from Baudouin to Yanmar. Compared to one and five years ago, as a percentage of vessels available for sale, there was a moderate increase in those powered by CATs, offset by significant decreases in those powered by Cummins, GM/DDs and MAN/MAN-B&Ws.

Marcon Broker's Comments

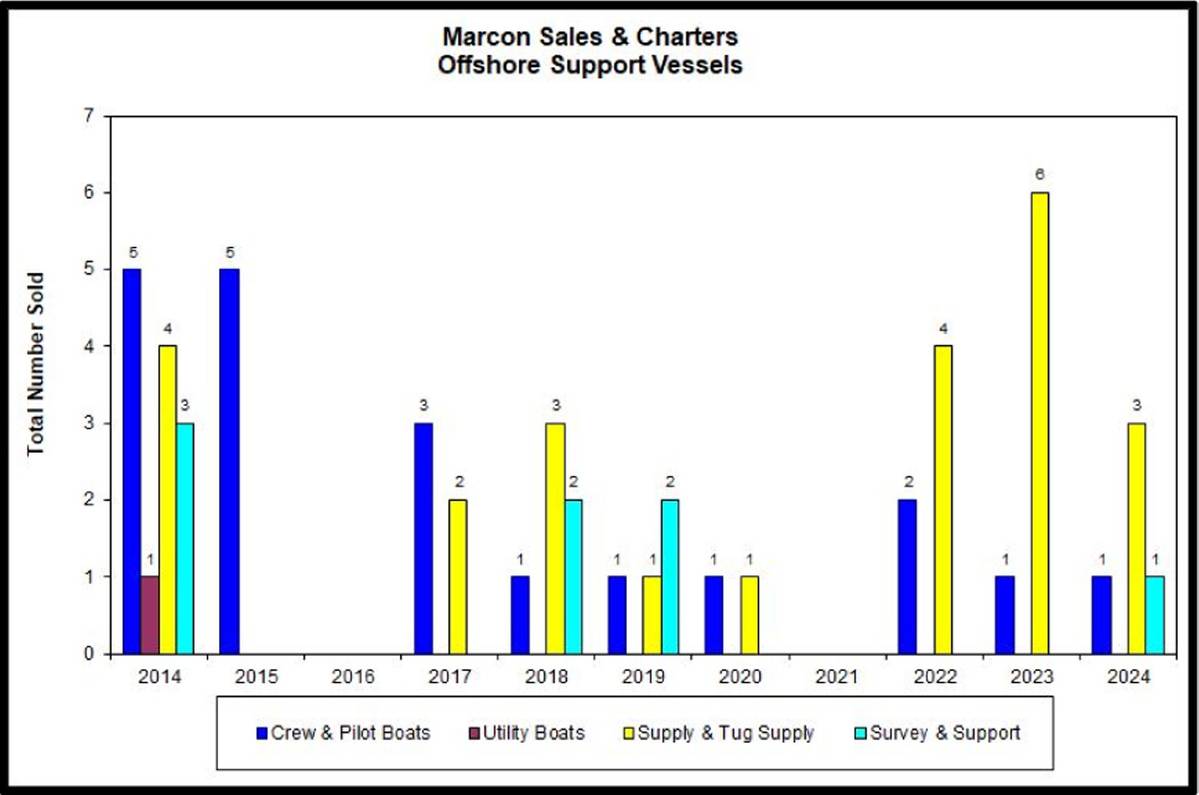

Overall, 2024 started slow for Marcon with very few sales in the first few months of the year. While we initially thought it was just us, in discussions with other brokers, we found it was across the board. However, as we hit mid-2024 and then third quarter 2024, there has been a serious turnaround with Marcon having multiple deals in various stages and indications of that continuing into 2025.

The Offshore Support Vessel (OSV) market in 2024 has experienced significant changes. According to market resources, it is reported that offshore newbuild prices have nearly doubled in three years, with large anchor handling tug supply (AHTS) vessels increasing by 97% and platform supply vessels (PSVs) by 67% since 2021. This surge in prices is supported by a low order book, indicating limited new vessel construction. Despite this, OSV rates have reached all-time highs throughout 2024, driven by increased demand and high vessel utilization. The demand for OSVs has risen by 2% year-over-year and 30% since the 2020 low, with utilization reaching 75%. Marcon has seen these changes in sales prices and charter rates firsthand, as well as the lack of availability depending on the specific market.

Investment opportunities in the OSV market have also become more attractive. Offshore support vessels, particularly PSVs and anchor handlers, are considered the best investment in shipping, offering high returns when bought secondhand, chartered, and then sold. This environment presents a lucrative opportunity for investors, even amid the challenging landscape. The sector's remarkable recovery and the robust demand for OSVs signal a positive trajectory for potential gains.

However, the OSV sector is not without its challenges. Financing for newbuilds, upgrades, and fleet renewal remains a critical hurdle. With owners needing funds to sustain and modernize their fleets, securing adequate financing has become pivotal. Additionally, new EU regulations and the inclusion of OSVs in the Emissions Trading System (ETS) starting in 2027 will increase operational costs and require investments in new technologies. These regulations, aimed at reducing emissions, will necessitate significant adjustments in operations and compliance efforts.

Furthermore, regional dynamics and market specifics play a crucial role. In Asia, demand for OSVs has surged due to increased spending by energy companies on new hydrocarbon projects and maintenance of offshore infrastructure. Meanwhile, the North Sea has seen rising day rates for Platform Supply Vessels (PSVs) and significant increases for Anchor-Handling Tug Supply (AHTS) vessels on the Norwegian continental shelf. Despite these favorable market conditions, the sector must navigate the complexities of financing, regulatory changes, and the need for technological advancements to ensure sustained growth and competitiveness.

The significant price increases and strong OSV rates highlight the market's response to limited new vessel construction and increased demand. A recent industry article discusses the OSV newbuilding market nearing a 'tipping point,' suggesting a critical juncture for future growth. Additionally, Tidewater's Q2 2024 report notes sequential increases in day rates, emphasizing the ongoing recovery and robust drilling prospects. The industry's fundamentals appear strong, with expectations for continued improvement through 2025.

In conclusion, the OSV market in 2024 is characterized by high demand, rising prices, and significant investment opportunities, tempered by challenges in financing and regulatory compliance. The outlook for 2025 remains positive, particularly in regions like Asia and the Gulf of Mexico, where activity is expected to increase. As OSV owners navigate these complexities, the focus will be on modernizing fleets, complying with new regulations, and capitalizing on favorable market conditions to sustain growth and profitability.

www.marcon.com / Commercial Marine Brokers since 1981